6 Tips for Cultivating Healthcare Savings Mentality in Consumers

Published on August 30th, 2016

The movement toward cultivating a healthcare savings mentality is still very much in its infancy. While there is a lot of work to be done to help consumers better understand the benefits of HSAs and to guide them toward better investment strategies, market trends show there is a huge opportunity for health plan administrators and employers to take a proactive approach to provide advice and education that will increase consumer confidence in healthcare savings.

Whether or not consumers wish to engage in health savings conversations, the bus has already left the station. Out-of-pocket costs for consumers, including deductibles and premiums, have continued to outpace wages over the last five years. Add to that expenses projected to be incurred after age 55, and it becomes clear that HSAs offer a unique advantage over traditional retirement savings accounts. Consumers attempting to navigate the rules, regulations and workings of HSAs, however, often get overwhelmed, leading to overall low adoption.

We’ve identified six ways health plan administrators and employers can help cultivate a healthcare savings mentality to drive adoption.

1. Position plans and accounts as a bundled benefit offering

Every plan should be paired with an HSA account, not just high deductible health plans (HDHPs). While consumers feel healthcare-related expenses more acutely with HDHPs, all plans involve some level of out-of-pocket expense.

The tricky conversation to navigate is explaining how plans and HSAs work together, while creating a separation of the insurance component from the savings component in the consumer’s mind. HSA conversations should revolve around savings, not just healthcare. According the U.S. Department of Labor, healthcare is the second largest annual household expenditure after housing. Painting a picture that explains the importance of saving for current and future healthcare expenses framed the same way as other essential living expenses can help shift the way consumers think about healthcare savings.

2. Offer tools & guidance to help consumers identify saving targets

Much of the current communication about HSAs revolves around plan features as opposed to funding recommendations. Because HSAs are a relatively new concept for consumers, another roadblock to adoption is an inability to accurately project how much to set aside for present and future needs. Offering a combination of digital and in-person resources is essential to improving consumer confidence (more on that later).

At the most basic level, contribution limits may serve as a guide, but most consumers just dipping their toes in may wish to begin with lower funding. Customized tools and guidance that make scenarios relevant to them will be most useful. One such tool is an online savings calculator or wizard which runs consumers through some easy-to-answer questions and then makes a suggestion for how much to contribute to the HSA.

Another option is to offer guidance and worksheets that walk the consumer through examining previous-year expenditures, as well as projected expenses for the coming year. It’s also helpful to make sure consumers understand that, unlike FSAs, HSA funds are not “use it or lose it” and can move from employer to employer. This may help alleviate some of the apprehension around funding levels.

3. Focus on the long term, not just this year

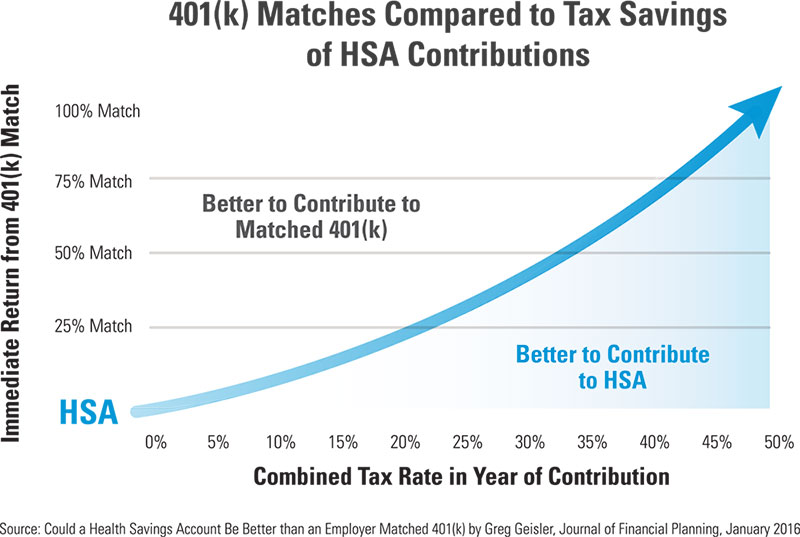

With so much focus on retirement funds, it can be hard to get the message out about the power of HSAs – not just as a complement to employer-based insurance, but as a long term investment vehicle itself. In fact, as the tax rate increases, the tax savings from HSAs outpaces the rate of return from 401k matching.

It’s essential that plan administrators and employers educate consumers on the value propositions of HSAs compared to FSAs and traditional retirement vehicles. One unique factor is that an HSA is the only investment that helps employees plan and provide protection for working-life years, as well as post-work years. Consumers must understand that they will not lose HSA funds at the end of the year and that the funds are portable.

It’s also vital to explain the “triple tax savings” associated with HSAs. A HSA is the only investment vehicle where neither the money in nor the money out is taxed when used for qualified expenses. Additionally, after age 65, funds can be withdrawn for any purpose. Though subject to taxation, this differs in no way from current retirement investment vehicles. A simple example underscores the tax advantage of HSAs: Someone over age 65 and in the 25% tax bracket incurring $4,000 in medical expenses for the year would have to withdraw $5,000 from a 401k or IRA to cover the expense and the tax. With the HSA, that same consumer could withdraw the $4,000 with no taxation. Going over examples like this with consumers should help them understand there is virtually nothing to lose by dedicating funding to an HSA.

4. Help consumers visualize outcomes and savings potential

In addition to providing tools for consumers to help determine the right level of funding, health plan administrators and employers should provide easy-to-follow graphics and charts that illustrate potential benefits.

Charts and graphs that show the following can help simplify complex and potentially daunting concepts:

- How tax savings increase with increased funding over time

- How pre-tax savings combined with funding for out-of-pocket expenses can have a net-positive impact on take-home pay

- How HSA withdrawals after retirement can provide greater tax savings than 401ks or IRAs

5. Don’t overlook the importance of human interaction

While many consumers today have an overwhelming preference for receiving information over digital channels, research actually indicates that the lower the consumer confidence level in a concept, the greater the desire for human interaction for learning and decision making.

With the leap straight into self-service digital distribution of information relating to HSAs, there may be a lot of missed opportunity on the table. There will always be early adopters, but for older consumers or those having trouble committing to the concept, your mix of education and training should include such things as:

- A telephone support hotline

- Webinars

- Lunch and Learns

- In-person enrollment with an advisor

As HSAs mature and consumer confidence increases, expect a greater gravitation toward digital channels, but the industry must first do the work of educating and advising consumers in order to reap the benefits.

6. Move beyond open enrollment by offering year-round education & support

In addition to communicating with consumers via their preferred channels, you must also be available with support and information at various times throughout the year.

The best strategy is one that charts the lifecycle of the HSA consumer at the following stages:

- Pre-enrollment – Provide education and training that builds general fluency

- Open enrollment – Help consumers compare options and make an informed decision

- Welcome & Onboarding – Provide practical information that sets the consumer up for a successful outcome

- Optimization – Check in with consumers to help them make course corrections that ensure an optimal experience

- Usage – Continue to drive incremental enrollment, funding and usage through education and advice

HSAs have been steadily gaining traction with consumers as the number of accounts and funding continues to increase year over year, with funding projected to increase another $17B by 2018 from $34.7B to $52B, according to Devenir. The numbers also show a high level of engagement and satisfaction among consumer-directed healthcare participants. By implementing these six best practices, cultivating the right mindset among consumers could help drive adoption and funding even higher.