How To Work With Employers to Grow Your CDH Programs

Published on December 5th, 2018

When it comes to growing a consumer-driven healthcare (CDH) program, there are plenty of moving parts. Most importantly, there are entities downstream that play a significant part in the success of your programs.

In our last post on the topic, we looked at how you – as a TPA or health plan – can grow your CDH programs by working with brokers to guide employers and consumers towards account-based plans. We’d be remiss, though, if we didn’t highlight the importance of direct employer engagement.

Employers play perhaps the most important role in the creation, marketing, and communication of health plans, and you should do everything you can to ensure they guide employees in the right direction.

The problem won’t fix itself

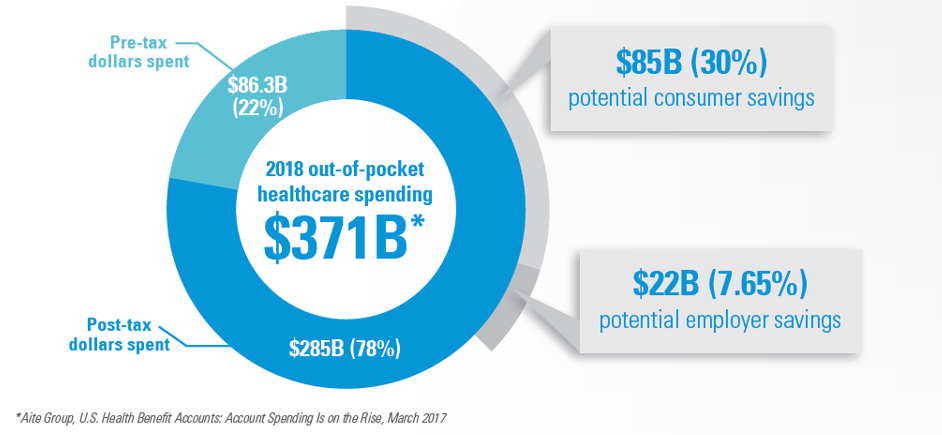

Adoption of CDH programs is improving, but at the same time, these accounts continue to be under-utilized and under-funded. This year, out of the $371 billion estimated to be spent on out-of-pocket healthcare expenses, just 22 percent ($82.6 billion) flowed through tax-advantaged CDH accounts.

By not taking advantage of CDH accounts like FSAs, HSAs, and HRAs, U.S. consumers are leaving a massive $85 billion in savings on the table, and employers are missing out on a further $22 billion. As an industry, we have a lot of work to do to bridge that gap.

But, here’s the thing. We can’t do it on our own. Even with brokers’ help, bridging that $107 billion gap isn’t easy.

So, here’s the first thing to remember: Employer decisions have a huge impact on the success (or failure) of CDH plans. If they make good decisions about the structure and availability of plans and provide employees with strong educational resources backed with consistent communication, CDH plans see outstanding levels of adoption. On the other hand, if they make poor decisions and neglect education and communication, employees are far more likely to stick with what they know.

Two golden rules for CDH plan adoption

When it comes to working with employers, there are two primary things that must be communicated in order to improve adoption of CHD plans:

1. Every health plan should be paired with an account

Practically every health plan comes with some out-of-pocket responsibility for consumer; therefore, when employers think about CDH, they should be thinking about more than just high deductible health plans (HDHPs) and health savings accounts (HSAs).

When communicating with employer groups, try to coach them to think about health benefit accounts more broadly and help them find ways to include them in all plan types. For example:

- Pairing traditional plans with an FSA

- Pairing high-deductible plans with an HRA or HSA

In an ideal future, we want to see all out-of-pocket spending flow through tax-advantaged accounts, because that’s what’s going to help save money for consumers and employers and also help shift consumer focus towards CDH plans in general.

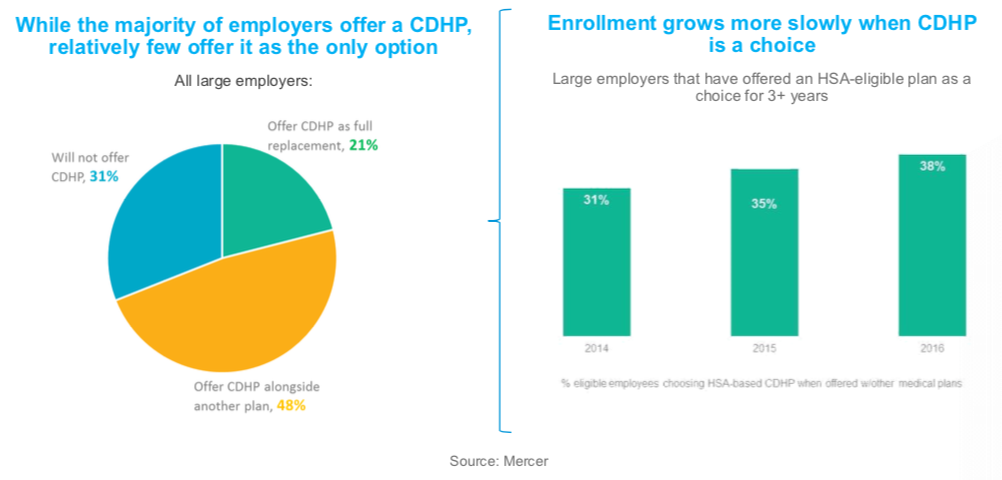

2. CDH plans shouldn’t be offered as a choice

When consumers have the option to choose between a CDH plan and one or more traditional plans, enrollment in CDH plans grows more slowly. In order for enrollment to increase, employers must “steer” consumers using incentives, good plan design, strong communication, and so on.

That might seem like an obvious point to make, but it actually highlights what could be a very important shift in thinking for employers. Right now, only 21 percent of employers are offering CDH plans as a full replacement for traditional plan types. If employers can be convinced to retire legacy plan types and only offer CDH plans, enrollment will naturally rise much more quickly.

In order for that to happen, though, you’ll need to encourage your employer groups to take CDH more seriously and to help them understand the value (both for them and their employees) that CDH plans and paired accounts have to offer.

Get a seat at the table

Of course, while these two approaches can have a substantial impact on CDH plan adoption, they aren’t the only considerations. There are many forces at play when it comes time for consumers to select a health plan, and you can’t expect a single change in tactics to massively increase adoption.

At the same time, you can’t sit back and let others control your destiny. Certainly brokers have a part to play in guiding employers towards improved CDH plan enrollment, but if you really want to grow your programs, it’s essential that you have a seat at the table when employers are making vital decisions about their health plan offerings.

If you don’t yet have that type of relationship with your employer groups, getting a seat at the table should be your number one priority.

Five factors that influence plan adoption

Once you have a seat at the table, or at least strong communication channels with your employer groups, there are five main factors that can be adjusted to maximize CDH plan adoption.

1. Plan design

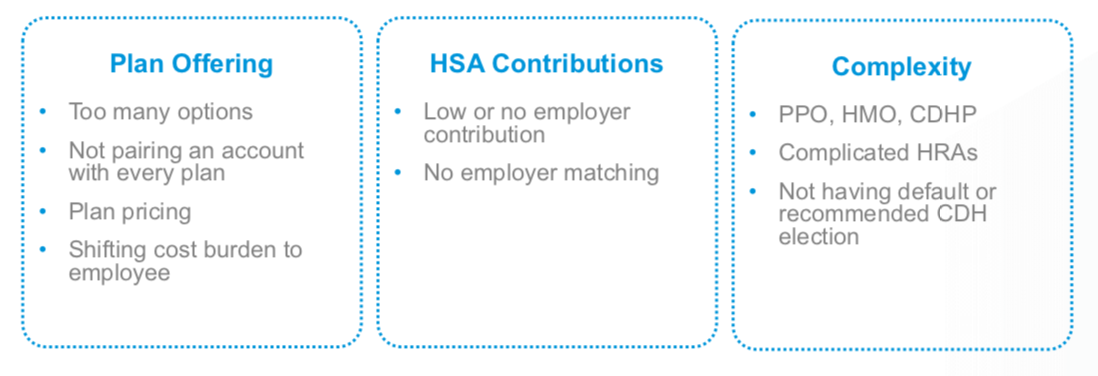

Again, this might seem obvious, but consumers will only choose CDH plans if they are put together well. Poor plan design only serves to weaken CDH offerings and does nothing to incentivize consumers to shift away from traditional plan types. Common issues with plan design include:

What makes a good CDH plan? First and foremost, they must be designed to benefit everybody. Plans that purely shift costs, while attractive to employers, will only alienate employees.

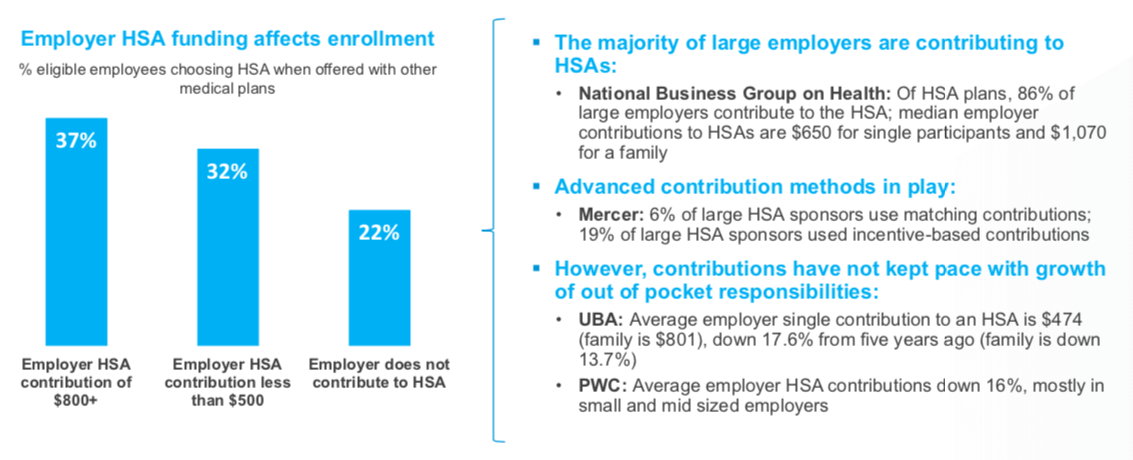

And, how do you make a CDH plan attractive? Simple: Convince employers to contribute to paired accounts. The evidence is clear, when employers contribute to health benefit accounts, enrollment increases dramatically.

Other important things to note are that all CDH plans should be paired with a suitable tax-advantaged account, offer at least some level of employer contribution, and be easy to understand.

2. Incentives

Sticking with the most obvious factors first, incentives can play an important role in increasing adoption of CDH plans. By all means employers should use strong incentives to help shift employee choices and behaviors, but it’s important to remember that incentives shouldn’t be used to the exclusion of other factors.

3. Environmental factors

Inertia is an extremely powerful force, which many people find almost impossible to overcome. In order to convince employees to select CDH plans, which will likely be very different to the traditional plan types they are accustomed to, old-school passive enrollment processes must be replaced with active alternatives.

So, what does that mean in practice? Each time open enrollment comes around, every employee must examine their options, and actively make their selection. At the same time, employers should be encouraged to remove legacy plan designs altogether and steer employee decision-making with a mixture of advocacy and incentives.

This disruption of the status quo helps avoid the inertia trap and also helps to improve employee understanding of and participation in their chosen health plans.

4. Education & decision support

Clearly, employees can’t be expected to choose CDH plans if they aren’t being provided with strong education and decision support tools. But, at the same time, how can employers be expected to provide those resources unless they too are being supported to do so?

Don’t forget, employers – specifically HR and personnel departments – are on the front line answering employee questions and steering the decision-making process. By supplying employers with strong education and decision support, you will help steer employees toward account-based programs.

5. Communication… and year-round reinforcement

We’ve talked about the importance of communication many times in the past… and for good reason. Informative, well-constructed, year-round communication strategies have a profound impact on CDH plan uptake and help raise employee fluency levels across the board.

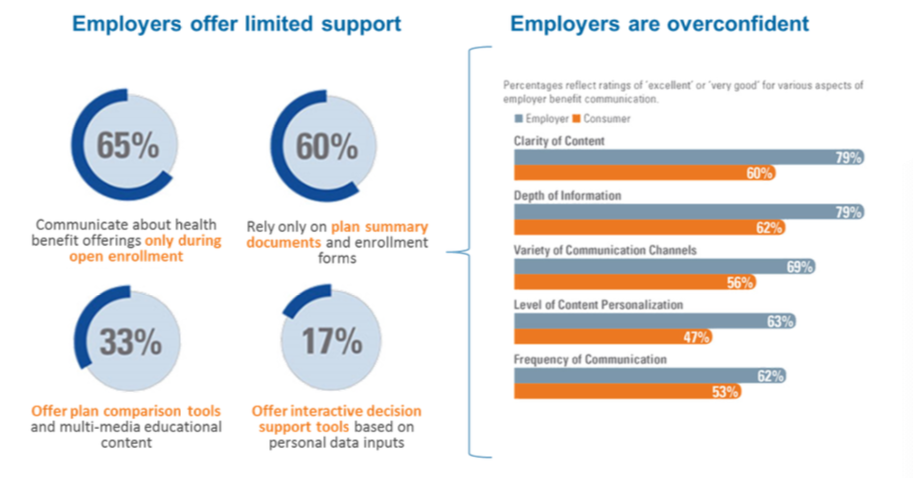

But, are your employer groups performing in this area? Do they communicate with employees about their plans year-round or just during open enrollment? Do they provide interactive decision support tools or simply rely on summary plan documents?

After a lot of research in this area, we can tell you this much: employer communications often miss the mark and many employers are overconfident about the effectiveness of their existing communication strategy.

To help mitigate the problems caused by poor communications, do everything you can to insert yourself into employers’ communications strategies. Instead of relying on them to develop their own resources, provide them with the help, support, and tools they need to radically improve employee fluency, and steer decision making towards CDH plans.

Remember, employers have knowledge gaps too

If you are already involved with your employer groups’ CDH plan strategy, you can start to apply some of the ideas from this post right away.

But, if you don’t currently have this level of involvement, it’s important that you don’t assume that your help simply isn’t welcome. Many employers would appreciate your guidance and support, particularly when it aligns with their business objectives.

To get your foot in the door, interact with your employer groups, and make sure you understand what they’re trying to achieve. Once you have some level of involvement, help them understand how important factors, like plan design and communications, influence enrollment and participation in their CDH plans.

Ultimately, even if you aren’t involved with initial pan design discussions, it’s worth doing everything you can to communicate with employers and try to find areas where you can add value. After all, if employers believe you can help them realize their business objectives, they are far more likely to welcome your involvement in their health benefit programs.