Q&A with Aite Group: Trends, Momentum, and Innovations in Health Benefit Accounts

Published on October 28th, 2016

Over the last decade, the healthcare market has shifted towards consumerism in a big way.

According to Mercer, almost three quarters of large employers will offer a consumer directed health plan (CDHP) by 2019, up from just 20% in 2009. And, as the CDH market continues to evolve, health benefit accounts have gained rapid traction.

This rapid rate of change prompts a variety of questions:

What does the future hold for account-based benefit programs? What growth can we expect? And what market forces are at play?

To shed some light on these questions (and more) Mike Trilli, Research Director at Aite Group, joined us for a rapid fire Q&A webinar. In this post we’ll summarize Mike’s key insights.

How big is the health benefit account market right now? What changes are we seeing?

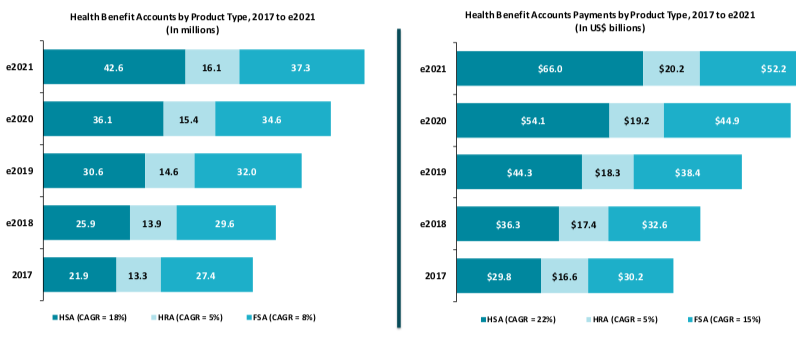

The most important thing to understand about the health benefit account market is that it’s seeing strong growth, and that isn’t about to change. Overall, health benefit account ownership is predicted to rise at a compound average growth rate (CAGR) of 11% between 2017 and 2021.

A sizeable portion of that growth is accounted for by HSAs, where ownership is anticipated to grow at a CAGR of 18% over the same period. Meanwhile, ownership of HRAs and FSAs will continue to rise, but at a much more sedate pace.

But of course, total accounts isn’t the only metric to consider: We also need to understand how the volume of payments made from health benefit accounts is changing.

Once again, HSAs lead the way with a massive anticipated CAGR of 22%, but FSAs are also expected to see a substantial increase in outgoing payments. According to Aite Group research, this is likely due to a modest increase in FSA contributions from both account holders and employers.

Another factor highlighted during the webinar was the role played by debit cards: Aite Group estimates that debit cards now account for 55% of all health benefit account payments, compared to 40% three years ago.

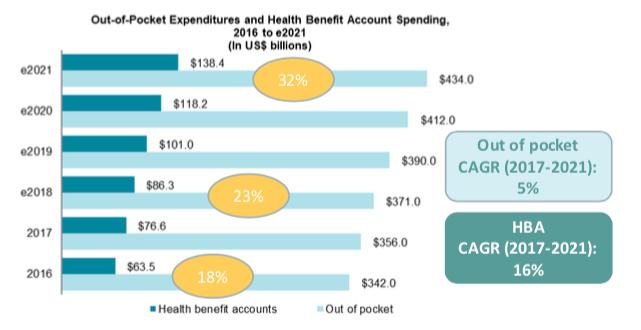

How does health benefit account spending compare to total out-of-pocket spending?

For many in the CDH world, the gap between out-of-pocket expenditure and health benefit account spending constitutes a huge opportunity. After all, they offer substantial tax benefits to consumers by enabling them to use pre-tax instead of post-tax dollars, which should make them an “easy sell.”

Accordingly, benefit account spending has risen as a proportion of out-of-pocket spending in recent years and is predicted to continue rising. While total out-of-pocket spending is anticipated to grow at a CAGR of just 5%, benefit account spending will grow at 16%.

Still, there’s a long way to go. So what can insurance carriers, brokers, and administrators do to continue bridging the gap? According to Aite Group, consumer education is the key.

On the webinar, Mike explained consumers need to understand the real financial impact of dollars saved in different accounts. For example:

- How much would consumers save on average by using pre-tax dollars for out-of-pocket expenses instead of post-tax dollars?

- In terms of investment, what is the value of a dollar in an HSA compared to a 401(k)?

If consumers can easily understand the financial impact of health benefit accounts, there will be a natural shift towards using them.

What big regulatory changes (and proposals) are coming, and how might they affect the market?

As the consumer directed health market continues to evolve, there will be more and more regulatory input. Right now, there are at least six different legislative movements that will likely impact health benefit accounts:

- Increases to maximum contribution limits

- Bipartisan HSA Improvement Act

- Association health plans

- High Cost Plan Act (Cadillac Tax)

- Chronic Disease Management Act

- Expanded HSA availability outside of an HDHP

In particular, Mike drew attention to two of these issues:

- The “Cadillac Tax” The Cadillac Tax has represented a significant sales barrier over the past few years, with employers understandably worried about the financial impact it could have. However, now that implementation has been delayed until 2020 (and there’s even talk of repealing it altogether), Mike believes that sales barrier has diminished considerably.

- Expanded HSA availability outside HDHPs While this is really only a debate at the moment, Mike believes it represents a huge opportunity for the health benefit account market. As things stand, many people are “locked out” of HSAs, simply because they don’t have an HSA-eligible plan. If eligibility hurdles were to be lessened in the coming years, there would be even greater potential for growth in the HSA market.

What trends are we seeing in account uptake at the employer level?

While there has been (and will continue to be) a substantial overall shift towards health benefit accounts, there are some clear differences in approach between market segments:

- Small businesses (10-99 employees) Many small businesses are run by younger people, who are naturally more inclined towards consumer directed health plans. As a result, the small business sector represents a greenfield market for health benefit accounts and HDHPs.

- Middle market employers (100-999 employees) Mid-sized employers are in the process of moving away from managed care and towards HDHPs. According to Aite group research, the “total replacement” trend has abated, but there is still a strong trend towards healthcare consumerism.

- Large employers (1000-4999 employees) Traditionally an HRA-dominated market, large employers are increasingly moving towards HSAs. Even when large employers don’t decide to offer HSAs, they still opt to move away from HRAs.

- Corporates (5000+ employees) Many large corporations have offered HSA-eligible plans for several years, and they are now focused on increasing participation in their existing HSA programs.

What factors are important to continued growth in the market? How can companies differentiate themselves?

With the health benefit account market set for tremendous growth in the foreseeable future, it’s no surprise that industry players are taking a close interest. On the webinar, Mike highlighted several key areas to focus on, including:

- Education Education is always important in the CDH world. In particular, Mike believes companies that promote broker education and have established broker channels, are in a very strong position to capitalize over the next few years.

- Debit cards Debit cards already constitute 55% of health benefit account spending and that figure is only going to increase. Having a strong, well thought-out card strategy will be essential to capitalize on HSA growth.

- Financial services Providing financial services via health benefit accounts is a huge opportunity for providers to develop lasting relationships with consumers. While people change plans all the time, it’s much less convenient for them to change account providers.

What is the likely impact of the financial services industry becoming involved in the market?

While we are in the very early stages of financial services companies becoming involved in the health benefit account market, Mike believes there is a lot to be excited about. In particular, he expects the trend to:

- Convince health benefit account holders to consider investing

- Attract many new consumers to the health benefit account market

- Lead to innovation and the creation of new account features

But, while there are plenty of positives, Mike also believes we’ll see financial services companies experience a lot of the same challenges that banks have: understanding eligibility, plan design, and the lack of healthcare expertise.

What role do technology platforms play in the future of health benefit accounts?

Clearly, there are plenty of areas where technology platforms can aid in the management and continued expansion of health benefit accounts. As a starting point:

- Enrollment and eligibility

- Payroll and advanced funding

- Provider and Rx search

- Payment processing

- Bill payment

- Price transparency

- Account management

- Investment and retirement

But beyond these, Mike highlighted one key area where technology platforms can add huge value to health benefit plans: creating a personal, familiar experience for account holders.

More than anything else, consumers want to feel comfortable in the use and management of their accounts. Powerful, white-labelled technology platforms bring the best attributes of health benefit products into a single location and give consumers the experience of working with a consistent, familiar brand.

Watch the webinar for (much) more

If you’ve found this article useful, we highly recommend registering for our on-demand webinar. Mike Trilli, Research Director at Aite Group, joined us for a full hour of rapid-fire Q&A and covered much more than we’ve had space for here.

To hear everything Mike had to say, click here to watch our on-demand webinar, Rapid Fire Q&A: Trends, Momentum & Innovations Impacting CDH Accounts.